Derivatives Market FAQs

A Derivative is a financial instrument whose value is derived from the value of an underlying asset. The underlying asset can be equity shares or index, precious metals, commodities, currencies, interest rates etc. A derivative instrument does not have any independent value. Its value is always dependent on the underlying assets. Derivatives can be used either to minimize risk (hedging) or assume risk with the expectation of some positive pay-off or reward (speculation).

The following are some common types of derivatives:

- Forwards

- Futures

- Options

- Swaps

A call option gives the holder (buyer/ one who is long call), the right to buy a specified quantity of the underlying asset at the strike price on the expiration date. The seller (one who is short call) however, has the obligation to sell the underlying asset if the buyer of the call option decides to exercise his option to buy.

Example: An investor buys One European call option on Stock “A” at the strike price of $35.00 at a premium of $1.00. If the market price of Stock “A” on the day of expiry is more than $35.00, the option will be exercised. The investor will earn profits once the share price crosses $36.00 (Strike Price + Premium i.e., $35.00+$1.00).

Suppose stock price is $38.00, the option will be exercised and the investor will buy 1 share of Stock “A” from the seller of the option at $35.00 and sell it in the market at $38.00 making a profit of $2.00 {(Spot price – Strike price) – Premium}.

In another scenario, if at the time of expiry stock price falls below $35.00 say suppose it touches $30.00, the buyer of the call option will choose not to exercise his option. In this case the investor loses the premium ($1.00), paid which shall be the profit earned by the seller of the call option.

A Put option gives the holder (buyer/ one who is long put), the right to sell a specified quantity of the underlying asset at the strike price on or the expiry date. The seller of the put option (one who is short put) however, has the obligation to buy the underlying asset at the strike price if the buyer decides to exercise his option to sell.

Example: An investor buys one European Put option on Stock ‘B’ at the strike price of $3.00, at a premium of $0. 25. If the market price of Stock ‘B’, on the day of expiry is less than $ 3.00, the option can be exercised as it is ‘in the money’. The investor’s Break-even point is $2.75 (Strike Price – premium paid) i.e., the investor will earn profits if the market falls below $2.75.

Suppose stock price is $2.60, the buyer of the Put option immediately buys Stock ‘B’ from the market @ $2.60 & exercises his option selling the Stock ‘B’ at $3.00 to the option writer thus making a net profit of $0.15 {(Strike price – Spot Price) – Premium paid}.

In another scenario, if at the time of expiry, market price of Stock ‘B’ is $3.20; the buyer of the Put option will choose not to exercise his option to sell as he can sell in the market at a higher rate. In this case the investor loses the premium paid (i.e. $0.25), which shall be the profit earned by the seller of the Put option.

Open Interests is not the same as the traded volumes. Volumes are the quantity traded for a specific period and gives us an idea about the activity for that given period. Open interests are outstanding positions and hence tells us about the level of interest in a particular counter. Open interests tell us about the depth in the market.

The significant differences in Futures and Options are as under:

Futures are agreements/contracts to buy or sell a specified quantity of the underlying assets at a price agreed upon by the buyer and seller, on or before a specified time. Both the buyer and seller are obligated to buy/sell the underlying asset.

In case of options the buyer enjoys the right & not the obligation, to buy or sell the underlying asset.

Futures Contracts have a symmetric risk profile for both the buyer as well as the seller, whereas options have an asymmetric risk profile. In case of Options, for a buyer (or holder of the option), the downside is limited to the premium (option price) he has paid while the profits may be unlimited. For a seller or writer of an option, however, the downside is unlimited while profits are limited to the premium he has received from the buyer.

The Futures contracts prices are affected mainly by the prices of the underlying asset and interest rates. The prices of options are however; affected by prices of the underlying asset, time remaining for expiry of the contract, interest rate & volatility of the underlying asset.

A forward is a contractual agreement between two parties to buy/sell an underlying asset at a future date for a particular price that is pre‐decided on the date of contract. Both the contracting parties are committed and are obliged to honour the transaction irrespective of price of the underlying asset at the time of delivery. Since forwards are negotiated between two parties, the terms and conditions of contracts are customized. Forwards contracts are negotiated bilaterally between two parties in Over the counter (OTC) markets and are not traded on the Stock Exchange.

A futures contract is similar to a forward, except that the contract is made through an organized and regulated stock exchange rather than being negotiated directly between two parties.

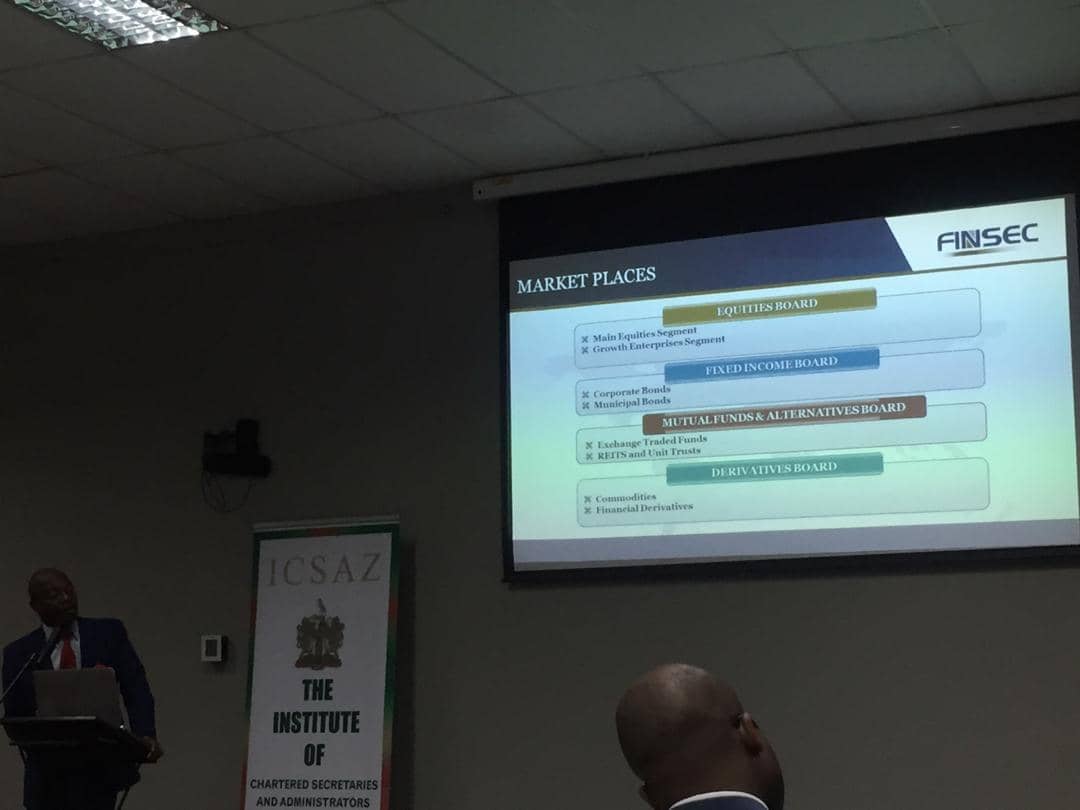

The following are some popular underlying asset classes on which Futures contracts exist:

- Equity

- Commodities

- Indices

- Currencies

Exchange Traded Markets – Exchange-traded Market is a platform where contracts are standardized, traded on organized exchanges with prices determined by the interaction of buyers and sellers through anonymous auction platform. A clearing house, guarantees contract performance (settlement of transactions).

Over the Counter (OTC markets) – Over the Counter (OTC) derivative contracts are signed between the two parties without going through the platform of a stock exchange or any other intermediary. OTC is the term used to refer stocks that trade through a separate dealer. These are well known as unlisted stocks where the securities are traded by broker-dealers through over the counter negotiations.

Expiration

Expiration (also known as maturity or expiry date) refers to the last trading day of the futures contract. After the expiry of a futures contract, final settlement and delivery is made according to the rules laid down by the exchange in the contract specifications document.

Contract Size

Contract size, or lot size, is the minimum tradable size of a contract. It is often one unit of the defined contract.

Initial Margin

Initial margin is the minimum collateral required by the exchange before a trader is allowed to take a position. Initial margins can be paid in various forms as laid down by the exchange and varies from assets to assets as well as from time to time. The level of initial margin is dependent on the price volatility of the contract. More volatile commodities generally have higher margin requirements.

Price Quotation

Price Quotation is the units in which the traded price of a contract is displayed. It can be different from the trading size of a contract and is often based on industry practices and conventions.

Tick Value

Tick Value refers to the minimum profit or loss that can arise from holding a position of one contract. Tick value depends on the size of the contract and its tick size. While it is often explicitly mentioned in contract specifications, it can be calculated by the formula:

Tick Value = Contract Size x Tick Size

Mark to Market

Mark to market refers to the process by which the exchange calculates and values all open positions according to pre-defined rules and regulations. Mark-to-market is an essential feature of exchange-traded futures contracts whereby the exchange ensures that all profit and losses are recognized by pricing them according to accurate market conditions. It is also an important feature for the risk management of positions of participants.

Delivery Date

Delivery date or delivery period refers to the time specified by the exchange during or by which the seller has to make delivery according to contract specifications and regulations. Delivery date is often later than expiry date of a contract, especially in case of physically delivered commodities.

Daily Settlement

Daily settlement refers to the process whereby the exchange debits and credits all accounts with daily profits and losses as calculated by the mark-to-market process.

Daily settlement is necessary in order to recover losses and pay profits to respective accounts.